The Fed’s Aggressive Monetary Policy Tightening: New Headwinds for Emerging Markets

As the COVID-19 pandemic enters its third year, emerging market economies will continue to struggle to improve their financial resilience in the face of numerous domestic and global headwinds. The emergence of new virus variants like Omicron serves as a stark reminder that the COVID-19 pandemic is far from over, and it could jeopardize the economic recovery prospects of both emerging and advanced economies.

First identified in Botswana and South Africa in November 2021, the highly-contagious Omicron variant is already wreaking havoc on a significant portion of the global economy in the near term, even though it appears to be less deadly than other variants. The recent spikes in COVID-19 infections are concerning in emerging market and developing economies (EMDEs) with significantly lower vaccination rates than the global average. Access to vaccines continues to be a stumbling block for most of these economies, leaving their populations more vulnerable to new virus variants. The economic consequences of relatively low vaccination rates in these economies are all too clear, with increased economic and financial crisis risks.

For most EMDEs and low-income countries (LICs), output and employment continue to be below pre-pandemic levels. Their fiscal situation has deteriorated rapidly since the pandemic’s outbreak. Due to their currencies’ low credibility, EMDEs and LICs have limited fiscal space in comparison to advanced economies. They, therefore, are unable to launch long-term recovery programs such as the EU’s Recovery and Resilience Facility and the US’s Build Back Better.

A Tough Landscape for EM Policymakers

In 2022, EMEs will face difficulties managing macroeconomic and financial stability in a highly unsettled global economic environment. This year, EMEs will continue to grapple with higher food and energy prices, persistent inflationary pressures, and supply-chain disruptions. Even if the global economy performs broadly in line with expectations, EMEs will face new challenges this year in bolstering their growth impulses and overcoming financial vulnerabilities.

In its latest Global Economic Prospects report, the World Bank forecasts that growth in EMEs will drop from 6.3 percent in 2021 to 4.6 percent in 2022 and 4.4 percent in 2023. The report notes that advanced economies’ output and investment will return to pre-pandemic levels next year, while EME output and investment will remain below pre-pandemic levels through 2023. “By 2023, all advanced economies will have fully recovered their output,” the report continues, “but output in emerging and developing economies will remain 4 percent below its pre-pandemic trend.” These forecasts by the World Bank indicate a growing disparity in growth rates between advanced and emerging economies, owing mainly to disparities in vaccination coverage and policy support by governments.

This year, three significant external headwinds for EMEs are: the tightening of monetary policy in the United States and other advanced economies; China’s slowing growth; and ongoing geopolitical tensions (especially US-China, US-Iran, and Ukraine-Russia).

Additionally, major elections will be held in 2022 in several emerging market countries (including Brazil, Colombia, Hungary, and the Philippines) amid a polarized political environment, lingering popular discontent, and widening economic inequalities. All of these developments could have a significant adverse effect on the outlook for EMEs.

This paper will focus on the prospect of a more aggressive normalization of monetary policy in the United States and its broader implications for EMEs in a financially interconnected world.

The Triple Threat of Policy Tightening

To contain the economic fallout of the COVID-19 pandemic, the Federal Reserve took a broad array of actions, including expansionary policy (slashing policy rates to near zero) and Quantitative Easing (large-scale buying of bonds and securities). The Fed has been purchasing $120 billion ($80 bn of treasury securities and $40 bn of mortgage-backed securities) every month since March 18, 2020, to support the US economy.

The Federal Reserve’s triple threat of policy tightening — tapering asset purchases, raising the target range for the federal funds rate, and shrinking its balance sheet — poses downside risks to a large number of EMDEs and LICs.

The tapering of the Fed’s asset-purchase program is the first significant step toward normalizing its ultra-loose monetary policy. After completing the tapering process, the Fed will initiate policy rate hikes. After that, the Fed would begin reducing the size of its balance sheet, a process known as quantitative tightening (QT).

The tapering process began in December 2021, with monthly asset purchases reduced from $120 billion to $105 billion. Surprisingly, within two weeks, the Fed decided to double the pace of tapering in response to rising inflation and a stronger economic recovery. On December 15, Fed Chairman Jeremy Powell announced that the Fed would reduce monthly asset purchases by $30 billion. As a result, the Fed’s net new bond purchases will be completely phased out in March 2022, three months ahead of the previous schedule.

Interest Rate Hike: Earlier and Faster

The US Fed has committed to maintaining interest rates near zero until inflation averages 2 percent over time, and maximum employment is achieved. Nonetheless, primarily due to inflationary pressures resulting from supply chain disruptions and high commodity prices, the Fed has taken a more hawkish stance in recent weeks, and thus could begin raising the federal fund rates even if the other goal of maximum employment had not been achieved fully.

According to the latest inflation data released by the US Bureau of Labor Statistics, the consumer price index increased by 7 percent in the 12 months ending December 2021, the highest 12-month increase since 1982. The upcoming employment cost index, which provides data on wage growth, could further add to the Federal Reserve’s pressure to usher in higher interest rates in early 2022.

With no signs of inflation abating soon, the Fed may hike rates four times in 2022, beginning in March, and another four times in 2023. The Fed’s December 14-15 meeting minutes indicate that its officials are willing to pursue much more aggressive policy tightening. The Federal Reserve’s so-called “dot plot,” which shows where each member of the Federal Open Market Committee (FOMC) believes interest rates should be in the coming years, revealed that a majority of FOMC members anticipate three rate hikes in 2022. While in September 2021, half of the FOMC members saw only one rate hike in 2022.

As the Federal Reserve sets the tone for global monetary policy, other systemically important central banks will follow suit. Except for the ECB and Bank of Japan, all major advanced economies’ central banks have either already raised policy rates or intend to do so in the first quarter of 2022. Since mid-2021, several large emerging market economies (including Brazil, Mexico, and Russia) have also raised interest rates primarily to contain domestic inflationary pressures and avert capital outflows.

Quantitative Tightening: Fast and Furious

Once the US Federal Reserve begins raising interest rates, its next move will be to reduce its bloated balance sheet, which currently stands at $8.7 trillion, or roughly 37 percent of GDP. Before the COVID-19 pandemic, its balance sheet represented approximately 20 percent of GDP.

The Fed could either initiate the QT immediately after the first rate hike or reduce its asset holdings gradually and predictably to avoid an unwelcome increase in bond and equity market volatility. For instance, the Fed may let some bonds run off the portfolio without reinvesting the principal at maturity.

There is an increased likelihood that the QT may start shortly after the first rate hike and will be more rapid than the last time. After the Fed began tapering in 2014, there was a two-year lag between the first rate hike and the start of the QT process. This time, the QT process is expected to be swifter as the Fed has already set up a permanent Standing Repo Facility to support the implementation of monetary policy and the smooth functioning of financial markets.

The minutes of the December meeting and comments by FOMC members suggest that the QT process may begin shortly after the rate increase cycle begins. Market analysts predict that the upcoming reduction in asset holdings will be more aggressive, likely totaling $750 billion per year.

The Spillover Effects of Policy Tightening on Emerging Markets

Given the dominant role of the US dollar in the international monetary system, the Federal Reserve’s aggressive stance towards monetary policy tightening could spell trouble for EMEs that are inextricably linked to global financial markets. Policy tightening would have direct negative ramifications for EMEs and LICs with open capital accounts, sizeable current account deficits, and high levels of external debt.

The financial channels would play a prominent role in generating negative spillovers to emerging markets. Hence, Latin American and Asian EMEs need to watch out due to their heavy reliance on dollar-denominated credit and increased “financial dollarization.”

A more hawkish policy stance by the Fed could be highly disruptive to emerging markets for several reasons. Firstly, an aggressive financial tightening would raise US yields and strengthen the US dollar against EM currencies. As a result, portfolio flows would abruptly reverse. The US-based global investors would pull money out of emerging markets and invest in “safe-haven” US assets, a la the infamous 2013 “taper tantrum.”

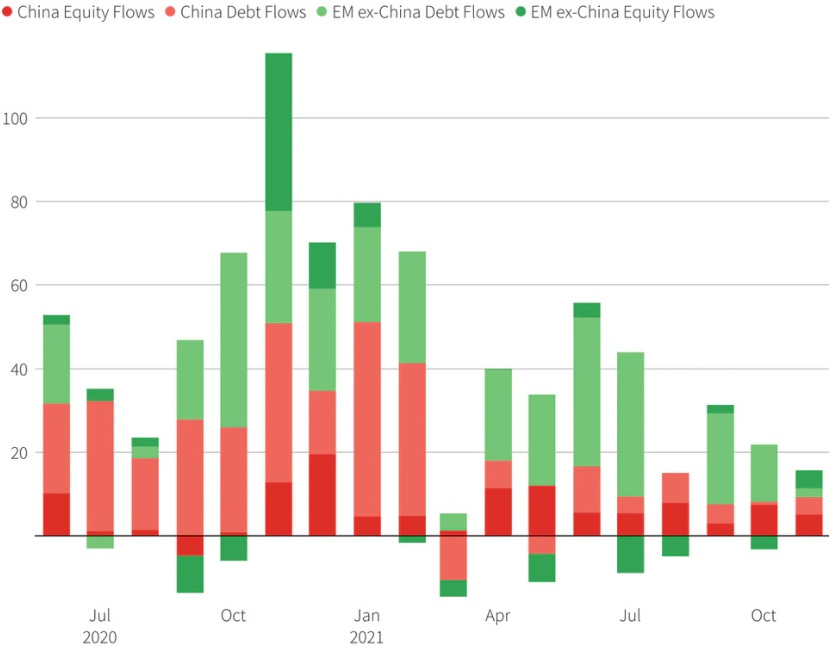

According to the Institute of International Finance’s Capital Flows Tracker, foreign investment in emerging market stocks and bonds (excluding China) has declined since December 2020, owing to concerns about the fragile economic recovery (Figure 1).

Figure 1: Non-resident EM Inflows by Destination and Asset Class ($ billion)

Source: IIF, Reuters.

The sudden stops and reversals of capital flows will lead to depreciation pressures on the EM currencies. When foreign investors invest in equities, bonds, and other financial assets in EMEs, they measure financial returns in US dollars and other foreign currencies. If the EM currency depreciates against the US dollar, it decreases the value of their investments in dollar terms and, therefore, they may engage in distress sales of funds. When foreign investors dump EM financial assets en masse in panic and move their capital to safe-haven assets (e.g., US treasury bonds), it creates more depreciation pressures on the EM currencies. A rapidly depreciating EM currency will likely prompt even more foreign investors to withdraw their money, as they fear the domestic currency will fall further. This could eventually result in a run on the domestic currency, perpetuating a currency crisis.

What about the impact on debt sustainability? The depreciation of domestic currencies would increase the stock of foreign exchange-denominated liabilities in domestic currency, complicating the debt sustainability of EMDE debt levels.

A depreciated currency would undoubtedly help boost exports, benefiting countries like Saudi Arabia and Iran that export energy, but would hurt countries like India, Indonesia, and Turkey that import oil and gas.

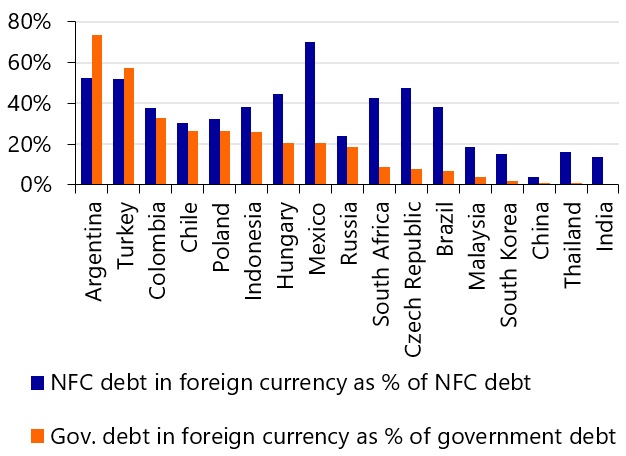

Secondly, EMDEs and LICs with a large stock of foreign currency debt and low forex reserves will be particularly vulnerable to tightening global financial conditions. This group of countries includes Argentina, Colombia, Indonesia, Turkey, and Sri Lanka. Figure 2 illustrates the share of foreign currency debt of governments and non-financial corporates (NFCs) in selected EMEs.

Figure 2: Share of Foreign Currency Debt of Governments and Non-financial Corporates

Source: IIF Global Debt Monitor, RaboResearch.

In 2020, six countries — Argentina, Ecuador, Belize, Lebanon, Suriname, and Zambia — have defaulted on their sovereign debt. Sri Lanka is next in the queue. Despite concluding currency swap agreements with China and India, Sri Lanka’s external liquidity is precarious due to annual foreign-currency obligations of $5-6 billion until 2025, and the country’s forex reserves (currently $1.5 billion) are dwindling to cover only a month’s imports.

Unlike in the 1980s and 90s, most emerging market borrowers (sovereigns and corporates) nowadays raise foreign currency debt via issuing bonds in the international capital markets dominated by giant asset management companies (AMCs). Due to their short-term and procyclical investment strategies, sizeable ownership of global AMCs in EME debt securities may result in significant bond price volatility and fire sales in reaction to tighter global financial conditions.

Thirdly, a rising US dollar would increase the debt-servicing costs (in local currencies) of EM NFCs with unhedged currency exposure, thereby exacerbating liquidity and solvency concerns. Even if EM NFCs use derivatives to hedge foreign exchange risks, they may still be exposed to significant liquidity risk due to maturity mismatches. Because of tighter global financial conditions, non-financial corporates from China, Brazil, India, and Mexico having significant refinancing needs during 2022-23 would face prohibitive costs while raising new dollar debt or rolling over their existing dollar debt.

Fourthly, in response to faster rate hikes by the Fed, EME central banks would have to raise interest rates to maintain interest rate differentials, prevent capital outflows and domestic currency depreciation, despite sluggish recovery and growth risks.

Indeed, tighter monetary policy by the US and other advanced economies presents dilemmas for policymakers in the EMEs. If EM central banks continue with the current loose monetary policy with low-interest rates, it will lead to capital outflows and domestic currency depreciation. On the other hand, if EM central banks pursue tighter monetary policy by increasing interest rates too early, it would derail a fragile domestic economic recovery. Hence, both options risk undermining the economic recovery process. Only those EMEs that actively manage capital accounts can pursue some degree of monetary autonomy.

Let us examine the complexity of possible spillover impacts of the Fed’s aggressive policy tightening on three emerging markets: Turkey, Indonesia, and India.

Turkey: Caught Between a Rock and a Hard Place

The financial tightening by the US Fed could further exacerbate Turkey’s external imbalances. Current economic imbalances have also been exacerbated by high inflation and the central bank’s procyclical monetary policy.

Turkey’s economy is particularly vulnerable to increased currency volatility and sudden stops due to its heavy reliance on foreign financing. While Turkey’s government debt is low by international standards, the majority of it is denominated in foreign currency, primarily the US dollar. The Turkish lira has lost nearly 40 percent of its value against the dollar since November 2021. The lira’s depreciation has exacerbated Turkey’s external vulnerabilities, as foreign currency debt now accounts for 60 percent of the central government’s debt, up from less than 40 percent in early 2018.

The weakening Turkish lira has increased pressure on domestic banks and non-financial corporates with a sizable foreign-currency debt. According to Fitch Ratings, Turkey’s external debt maturing by end-September 2022 amounts to $168 billion, the majority of which is held by banks and NFCs. Turkish banks’ only saving grace is that they hold substantial foreign currency deposits abroad. What is more concerning is that the lira’s depreciation would exacerbate the dollarization of deposits. At present, 56 percent of residents’ bank deposits are held in foreign currency and gold.

The Central Bank of Turkey (CBRT) recently concluded currency swap agreements with the People’s Bank of China and the Bank of Korea, and the IMF’s allocation of $6.3 billion in special drawing rights has aided in the country’s forex reserves expansion. However, the critical question remains: Are Turkey’s foreign exchange reserves sufficient to support a collapsing lira?

Over the last two years, the CBRT has conducted unannounced currency market interventions, spending tens of billions of dollars of its foreign exchange reserves to shore up the lira. Turkish President Recep Tayyip Erdogan stated in April 2021 that authorities had used $165 billion in central bank foreign-currency reserves to weather the 2019 and 2020 economic downturns. These large interventions did not help stem the lira’s fall, but they did deplete the country’s forex reserves. Turkey’s current gross foreign exchange reserves ($63 billion on January 7, 2022) are not large enough to prevent the lira from depreciating further. Worse, Reuters calculations indicate that Turkey’s net foreign exchange reserves — excluding funds exchanged through swaps with domestic banks and other central banks, as well as other liabilities — are negative.

Indonesia: Highly Vulnerable to Capital Reversals

Due to its heavy reliance on external funding, Indonesia is highly vulnerable to external financial shocks resulting from the Federal Reserve’s aggressive tightening of monetary policy. Unlike other Asian EMEs, Indonesia has been increasingly issuing foreign-currency bonds in the international capital markets in recent years.

In addition, the high dependence on portfolio inflows makes the country more vulnerable to market pressures caused by shifts in investor sentiment. Indonesia is among the top three EMEs with the highest participation of foreign investors in local currency bond markets (LCBMs). Before the COVID-19 pandemic, foreign investors held over 40 percent of local currency government bonds. Foreign investors currently own 37 percent of LCBMs, raising the prospect of large capital outflows if risk aversion suddenly rises.

Risk-off events, influenced by the US Federal Reserve’s tightening of monetary policy, would result in large capital outflows, exposing LCBMs to the risk of rising yields, while also putting strong downward pressure on the rupiah. Indonesia has experienced increased exchange rate volatility in previous episodes of global financial tightening, including the global financial crisis (2008), the “taper tantrum” (2013), and the COVID-19 crisis (2020).

The rupiah depreciation against the US dollar would automatically revalue the country’s external debt and the debt servicing costs in local currency, further limiting debt affordability. Increased funding costs would be disastrous for domestic corporations that borrow in US dollars from offshore bond markets without hedging their foreign currency exposure. For instance, Indonesian media and real estate firms borrow funds in US dollars, but their revenues are in rupiah. If foreign currency exposure is not hedged, the rupiah depreciation will negatively affect such firms’ liquidity and profitability.

Indonesia should reconsider its policy of allowing higher foreign participation in LCBMs. In this regard, the Indonesian authorities could learn from India’s regulations that set quantitative limits on foreign ownership of government and corporate bonds, an investment utilization limit, a minimum residual maturity of one year for corporate bonds, and concentration limits on single/group investor-wise in corporate bonds.

India: Are Forex Reserves Adequate to Cushion Against External Shocks?

It is important to note that the impact of capital reversals could be pronounced in India with limited capital account liberalization. The Indian rupee is not fully convertible on capital account. In India, portfolio flows into equity markets are unrestricted, but they are subject to sectoral caps and macroprudential restrictions in debt markets.

The fast accumulation of forex reserves in recent years has made India the fourth-largest forex reserves holder in the world after China, Japan, and Switzerland. India’s forex reserves currently stand at $632 billion, with an import cover of 15 months. Many analysts believe that India’s huge forex reserves would be sufficient to address capital flight and currency depreciation in response to tighter monetary policy by the Fed. That may not be the case if we assess forex reserves in relation to external liabilities.

To better gauge India’s external vulnerabilities, let’s begin with short-term external debt liabilities. India’s external debt worth $256 billion will mature over the next 12 months, according to the September 2021 data released by the Ministry of Finance. Non-financial corporations alone account for $128 billion, according to the data. To put this in context, India’s total external debt maturing until September 2022 accounts for 40 percent of the country’s forex reserves.

Second, India’s negative net international investment position (the difference between foreign assets and liabilities) of $331 billion as of September 2021 is a cause for concern if sudden stop events materialize.

Third, according to National Securities Depository Limited data on foreign portfolio investments, US-domiciled funds own up to 38.5 percent of Indian equities, accounting for $246 billion of the $640 billion total equity portfolio of FPIs in November 2021. Rapid selloffs by US-based funds would put downward pressure on the rupee, as foreign investors would convert their equity investments in the rupee to the US dollar. The rupee depreciation would also result in imported inflation as India relies heavily on oil imports to meet domestic demand.

Suppose large capital outflows from equity markets occur due to the Fed’s tighter monetary policy stance, combined with significant debt repayments and rising international crude oil prices. In that scenario, India’s massive forex reserves may be insufficient to contain downward pressures on the rupee and protect the domestic economy from large outflows.

In such a scenario, Indian non-financial corporates with substantial US dollar debt must also watch out, as their share of the country’s total external debt is a whopping 36.9 percent. Indian corporates that have not hedged their foreign currency borrowings may face higher foreign currency funding costs, as well as liquidity and solvency risks.

Whither International Cooperation?

In an ideal world, swift international policy coordination would manage the spillover effects of monetary policy normalization in the US and other advanced economies. Policy coordination among emerging and advanced economies would also help avoid spillbacks to advanced economies. Despite repeated calls by several emerging market central banks for some form of rules-based international monetary policy coordination in a financially interconnected world, the US Federal Reserve and other advanced central banks have overlooked such demands.

The second option is close collaboration between the US Fed and EMDE central banks in providing foreign currency swap lines to address potential dollar funding risks. The Fed has remained evasive in this regard as well. Even if not used, such dollar liquidity arrangements would enhance EM central banks’ credibility and financial market stability.

During the COVID-19 crisis, the US Fed offered temporary currency swap lines to only two EM central banks (of Brazil and Mexico). In 2021, the Fed established a new FIMA repo facility, which provides dollar liquidity to other foreign central banks (that do not have access to swap lines with the Fed) in exchange for US Treasury securities as collateral. Hence, EMEs have extremely limited access to both dollar funding mechanisms. Until now, the Fed has shown no willingness to extend these mechanisms to EMEs and LICs that do not have access to swap lines or a sufficient quantity of US Treasury securities to use the FIMA repo facility effectively.

Primarily due to the Fed’s selective approach, bilateral currency swap arrangements between EMEs have proliferated in recent years. In particular, the People’s Bank of China (the country’s central bank) has renewed or signed yuan-denominated currency swap agreements exceeding $500 billion with 35 EMEs and low-income countries (including Argentina, Turkey, Thailand, Pakistan, and Sri Lanka), more than any other country in the world. Intriguingly, Pakistan in 2013 and Argentina in 2014 used yuan-denominated swap agreements to obtain renminbi and convert it to US dollars in offshore markets during times of financial distress. No wonder, such flexible currency swap agreements also bolster China’s global economic influence, much to the displeasure of the US.

Given the IMF’s poor handling of previous financial crises, many EMDEs took steps to strengthen their first and second lines of defense — foreign exchange reserves and regional financing arrangements, respectively. Following the Asian financial crisis of 1997, many EMDEs have been accumulating large foreign exchange reserves to self-insure against volatile capital flows and other external shocks. While it is undeniable that large forex reserves bolster EM central banks’ ability to intervene in currency markets, holding large reserves entails fiscal costs.

Additionally, central bank interventions are considered most effective when conducted for a brief period (less than a month). Otherwise, central banks risk depleting substantial forex reserves without significant impact, as seen in China (2015) and Turkey (2019-20).

In the current scenario, several EMEs and LICs would be willing to seek greater financial assistance from the IMF and other multilateral financial institutions, provided such assistance does not come with harsh austerity measures. Since the pandemic outbreak, the IMF has provided new financing of $110 billion to 86 countries and allocated $650 billion in Special Drawing Rights (SDRs). While these are positive developments, dealing with external shocks will require far more financial resources, especially in systemically important emerging markets.

On the other hand, small economies may benefit from regional financial arrangements (such as the Chiang-Mai Initiative Multilateralisation, the Arab Monetary Fund, and the Latin American Reserve Fund), that can provide immediate assistance to member countries to alleviate US dollar liquidity pressures.

The Need for Swift Domestic Policy Action

The EMEs and low-income countries should initiate swift domestic policy responses to minimize the adverse effects of cross-border spillovers caused by tightening US monetary policy. Given that the US and other advanced economies have already begun the process of policy normalization, the next three months are critical for emerging market policymakers to take proactive measures to cushion the impact on domestic growth sources and insulate their economies from volatile capital flows.

While EMEs and low-income countries should tailor their response to their particular circumstances and vulnerabilities, macroprudential tools, capital controls, and currency-based measures are all examples of time-tested measures that can help prevent and mitigate external financial shocks. The challenge lies in designing an appropriate policy mix depending on the potential macroeconomic and financial risks.

In addition, EMDEs need to strengthen regulation and supervision of their financial sector to identify potential systemic risks and risk build-up in specific sectors. Their central banks should regularly monitor banks and NFCs to assess their foreign currency exposures and derivatives positions to limit system-wide financial risks.

Rethink Capital Account Liberalization

The financial crises of the past two decades have shifted the policy pendulum in the direction of capital controls. Controls on outflows could be prudent to prevent abrupt capital outflows and currency depreciation, as seen in Malaysia (1998), Iceland (2008), China (2016), and Argentina (2019). The controls on outflows are even more relevant for poor countries that do not have large foreign exchange reserves or access to currency swap lines and regional financing arrangements.

Available evidence suggests that countries that imposed tight capital controls recovered more quickly from the 2008 global financial crisis than those with an open capital account. As noted by the IMF economists, EMDEs that adopted tighter macroprudential policies and capital controls before the taper talk phase of 2013 coped better with the market pressures during the taper tantrum.

It is high time that EM policymakers rethink the costs and benefits of an open capital account. They should adopt a much more cautious approach towards capital account liberalization that involves the removal of controls, taxes, subsidies, and quantitative restrictions on capital account transactions. Under a liberal, open capital account regime, residents and non-residents can move capital and financial assets across borders without any restrictions.

As explained elsewhere by the author, the arguments supportive of capital account liberalization are highly overstated and backed by very little evidence. The evidence does not support the hypothesis that capital account liberalization generates higher rates of economic growth. A significant number of studies have found no causal relationships between capital account liberalization and economic growth, while the costs are increasingly evident in the form of recurrent financial crises in emerging markets. The IMF’s Ex-Post Evaluation of the 2018 Stand-By Arrangement with Argentina (released on December 22, 2021) also noted: “In Argentina’s recent economic experience, capital account liberalization favored the massive inflow of short-term speculative portfolio capital in 2016-2017 and left the economy extremely vulnerable to the event of a sudden stop, which effectively materialized in 2018. It also left the economy vulnerable to further volatility in the exchange rate, which fueled the inflationary process.”

South Korea’s Regulations on Forex Markets

South Korea’s regulations on forex markets are worthy of consideration to protect the domestic economy from speculative hot money flows. Based on lessons learned from two severe financial crises — the 1997 Asian financial crisis and the 2008 global financial crisis — the Bank of Korea (BoK) began implementing a series of measures to mitigate forex vulnerabilities and taming volatile capital flows in 2010.

In 2011, the BoK implemented a levy on banks’ non-core foreign exchange liabilities, requiring banks to pay a 0.2 percent foreign exchange stability levy on the balances of non-deposit foreign currency liabilities with a maturity of less than one year. The levy is applied uniformly to domestic banks and local branches of foreign banks operating in South Korea. Fifty-seven banks are subject to the levy. The funds raised through the levy are meant to provide emergency foreign currency liquidity to banks in times of distress.

The stability levy penalizes carry trades, in which banks borrow short-term foreign currency in order to convert it to Korean won and invest in domestic assets. From a financial stability viewpoint, the levy is intended to rein in excessive foreign borrowing and encourage banks to seek longer-maturity offshore debt, thereby mitigating the risk of shocks caused by rapid capital inflows and outflows.

Along with mandatory reserve requirements for foreign currency deposits, the BoK capped banks’ daily foreign exchange derivatives positions (the difference between foreign currency assets and liabilities) to prevent banks from building excessive FX derivatives positions, which were typically financed through short-term borrowing, thereby increasing maturity mismatches and financial vulnerability throughout the banking system.

With the three-pronged regulatory approach, the BoK accomplished its goal of containing the systemic risk from short-term forex borrowing by banks and taming volatile capital flows. These measures resulted in a significant decline in foreign banks’ forex derivatives positions and a major shift away from short-term forex funding and toward longer-term forex funding by foreign banks. The banks’ non-deposit foreign liabilities also decreased significantly. Interestingly, South Korea implemented these regulatory measures despite mounting criticism that they violate the OECD’s Codes of Liberalization of Capital Movements.

To summarize, monetary policy normalization is happening in the US. Recent developments indicate that the Federal Reserve is adopting an aggressive stance toward its monetary policy and is eyeing interest rate hikes early this year. The earlier and faster normalization of monetary policy by the US Fed increases the risks to macroeconomic and financial stability in emerging markets and low-income countries. In the absence of international policy coordination, their policymakers must make full use of the available policy levers to strengthen macroeconomic fundamentals and policy frameworks.

Image courtesy of 123rf.com